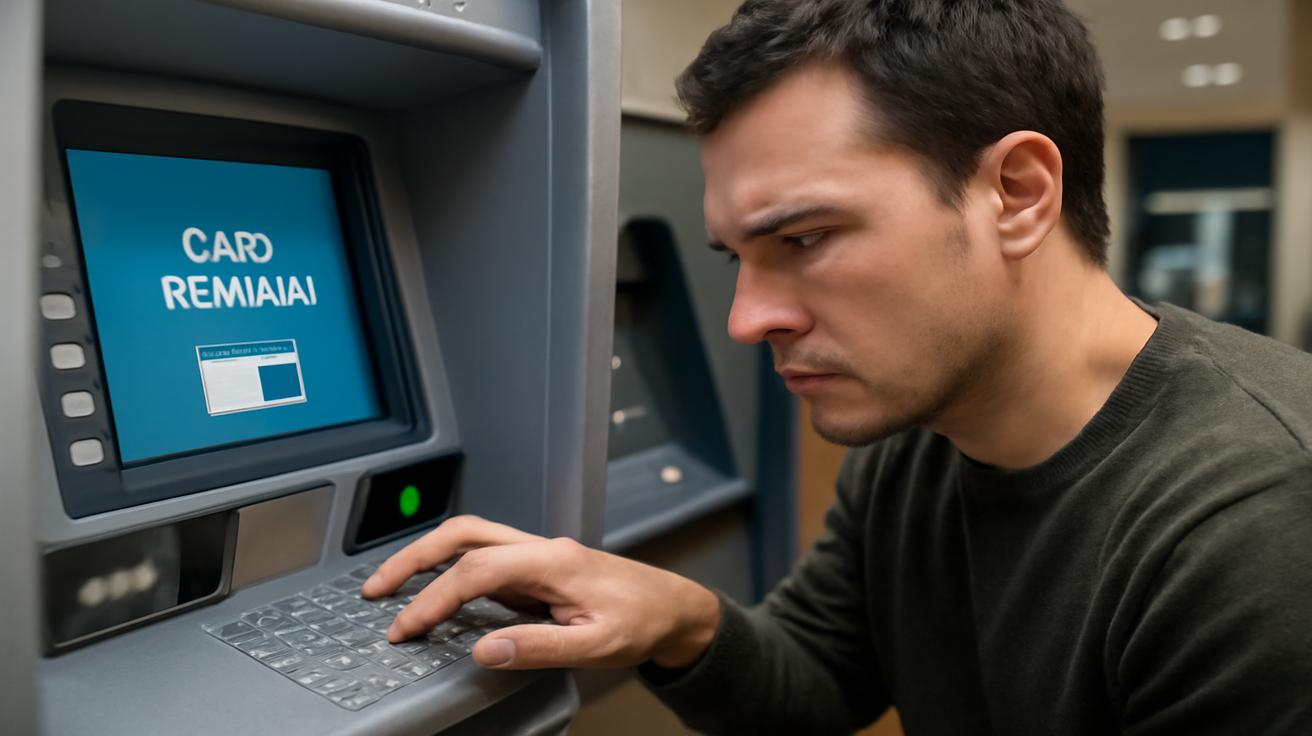

The afternoon light filtered through the glass doors of the shopping centre as you approached the familiar blue machine. Your mind wandered through the mundane details of your day—bills to pay, groceries to buy, nothing that demanded special attention. You inserted your card into the slot, entered your PIN, and waited for the familiar whirring sound of dispensed notes. But this time, something went wrong. The machine beeped. A message flickered across the screen. And then, silence. Your card had vanished inside the machine, swallowed by mechanisms you couldn’t see and couldn’t control.

Understanding Why ATMs Retain Cards

ATM card retention happens more frequently than most people realise. Financial institutions have programmed these machines to confiscate cards for several legitimate reasons. The most common trigger occurs when a customer enters an incorrect PIN multiple times in succession. After three failed attempts, the machine locks the transaction and captures the card as a security measure, preventing potential fraudsters from gaining access to your account.

However, card retention isn’t always triggered by user error. Technical malfunctions can cause the machine to malfunction at the final step, trapping your card inside. Expired cards sometimes trigger retention protocols, as do cards flagged for suspicious activity by your bank’s fraud detection systems. In rare instances, communication failures between the ATM and your bank’s servers can interrupt the card return cycle, leaving you standing there bewildered and card-less.

Damaged magnetic strips or embedded chips can also cause the machine to refuse returning your card. Modern ATMs scan cards thoroughly before processing transactions, and any irregularities in the card’s physical condition may prompt the machine to retain it as a safeguard against counterfeit cards.

Your First Actions Matter Most

The initial moments after your card disappears are crucial. Resist the urge to immediately strike the machine or demand it return what’s yours. Instead, take a deep breath and look at the screen carefully. Most ATMs display a message indicating why your card has been retained. Read this message thoroughly—it often contains important information about next steps.

Check if the machine offers a receipt option. Some ATMs will print a transaction record that includes a reference number, which proves you attempted to withdraw funds and can serve as evidence if disputes arise later. Document this reference number carefully, as your bank may require it when investigating the incident.

The Emergency Button: Your Hidden Lifeline

Few ATM users realise that most machines contain an emergency button or panic button designed precisely for situations like yours. This button typically appears prominently on the machine’s exterior, marked with a red alarm symbol or clearly labelled “EMERGENCY.” Look for it immediately—it’s usually positioned near the card slot or beside the screen.

Pressing this button connects you directly to the ATM operator’s customer service line through an integrated speaker system. A representative can monitor the situation in real-time and guide you through immediate recovery options. In some cases, they can remotely instruct the machine to eject your card. In others, they’ll collect your contact information and arrange for the card to be retrieved by authorised personnel.

Don’t hesitate to use this feature. ATM operators expect these calls and respond professionally. They’ll likely ask you to verify your identity using information only the cardholder would know—your full name, address, date of birth, and possibly the last few transactions on your account. This verification protects you from unauthorised access while confirming your legitimacy to retrieve your card.

Contacting Your Bank Immediately

Whether or not you successfully use the emergency button, contact your bank directly as soon as possible. Find the customer service number on your bank statement, official website, or the back of any other banking cards you may have. Many banks maintain 24-hour customer service lines specifically for situations involving retained cards or suspected fraud.

Inform the representative that your card has been retained by an ATM. Provide them with the machine’s location, the time the incident occurred, and any reference numbers the machine printed. This documentation creates an official record that protects you if unauthorised transactions occur while your card remains trapped inside the machine.

Your bank can immediately flag your account as potentially compromised and monitor it for suspicious activity. They’ll also initiate a procedure to retrieve your card from the ATM operator’s secure facility. Some banks can arrange for a replacement card to be sent to you within one business day, ensuring minimal disruption to your financial access.

What Happens to Your Card Inside the Machine

Understanding the security protocols surrounding retained cards provides reassurance during a stressful situation. When an ATM confiscates a card, it doesn’t simply fall into a random compartment where thieves can access it. Instead, the card drops into a secure vault within the machine that only authorised bank personnel can open using specialised keys and security codes.

The machine immediately locks and flags this event in its system. The next time a bank technician services the machine—typically within 24 to 48 hours—they retrieve the card from the secure vault and follow established procedures. Cards are never left unattended, and access is strictly controlled and logged.

Your bank maintains records connecting your card to the specific ATM and timestamp when it was retained. This creates an auditable trail that protects both you and the financial institution. Banks take this process seriously because mishandling retained cards damages customer trust and invites regulatory scrutiny.

Preventing Future Card Retention Incidents

Once you’ve recovered from this experience, take steps to prevent recurrence. If you entered an incorrect PIN, write your PIN in a secure location you can access—never on the card itself or in obvious places. Consider using a PIN you’ve used successfully for other accounts, something familiar enough that muscle memory prevents mistakes.

Check your card’s physical condition regularly. Cracks, bends, or visible wear on the magnetic strip can trigger retention protocols. If your card shows damage, contact your bank and request a replacement before attempting to use ATMs.

Keep your account in good standing and avoid transactions that might trigger fraud alerts. Unusual spending patterns or transactions in unexpected locations can prompt your bank’s security systems to restrict your card. If you travel, notify your bank in advance so international transactions don’t activate security blocks.

When to Consider Legal Action

In rare instances where a bank’s negligence causes financial harm—such as when a card is damaged during retrieval or when a bank fails to return a retained card within reasonable timeframes—you may have grounds to pursue compensation. Document everything: the incident date, times you contacted the bank, names of representatives you spoke with, and any financial losses you incurred due to lack of account access.

Contact your bank’s complaint department and file a formal grievance. If they don’t respond satisfactorily, escalate to your country’s financial ombudsman or banking regulatory authority. These organisations exist specifically to protect consumers when banks fall short of their obligations.

Moving Forward

A retained ATM card feels like a violation of trust, but it’s a manageable situation with straightforward solutions. By knowing about the emergency button, understanding proper notification procedures, and recognising the security measures protecting your card, you’ve already equipped yourself for future encounters. Most situations resolve within hours, and modern banking systems ensure your account remains protected throughout the process.

Leave a Comment